No one can tell you exactly what makes up your credit score. Well, except for the credit bureaus, and they’re not telling- it’s their “secret sauce.”

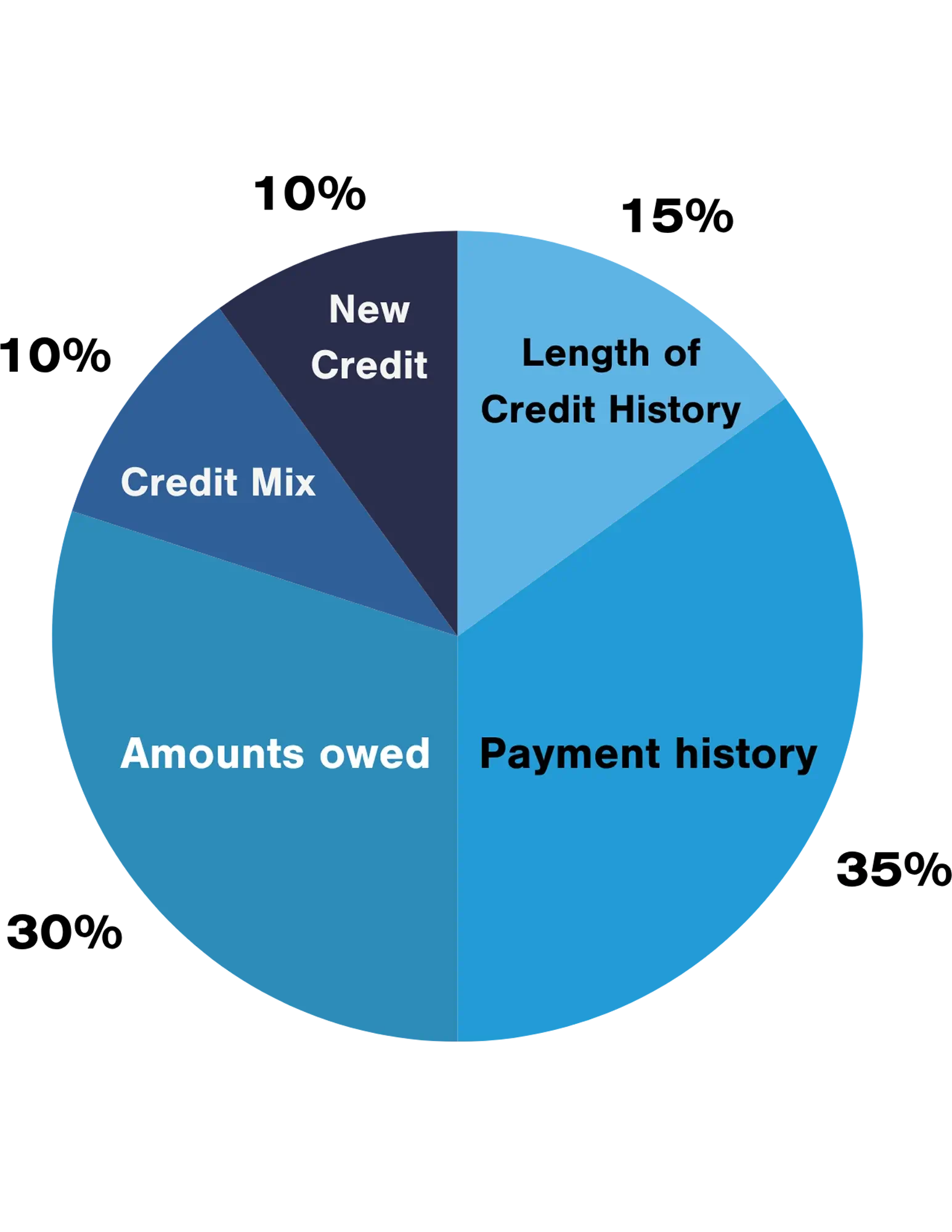

We do know however that your credit score is affected by five main areas. The FICO® Score—a standard credit scoring model used by many lenders—assigns a specific weight to each factor, as shown in the chart below.

- Payment history.

- Amounts owed.

- Length of credit history.

- New credit.

- Types of credit used.

Generally, there’s no quick way to build good credit or fix bad credit. Don’t get too discouraged though, within the time frame of a few months you can see measurable improvement in your credit score. And for those brand new to credit, it may take a few additional months for a score to show up in the first place.

Payment history: Making on-time and full payments to creditors is the most important thing.

Amounts owed: On loans like credit cards (a revolving loan) you should not use the full credit limit available to you. An example: if you have a $1,000 credit card limit and you have a $950 balance, you appear to be “maxed out”- this hurts your credit. For revolving loans, the general advice is to keep your balance below 30% of the limit.

On loans like car loans (an installment loan), the more you pay down on the balance from the original amount, the better. An example: if you borrowed $10,000 to buy a car and you have paid back $2,000, you still owe (with interest) more than 80% of the original loan. As you pay it down, your credit score improves.

Payment history and amounts owed make up most of your credit score. Focus most of your energy here.

Length of Credit History: In most cases, keeping credit accounts open is likely to help you, not hurt you. Closing older, lesser-used accounts can hurt your score by decreasing your length of history, as well as increase the percentage of your total credit you are using.

New credit: This includes the number of recent account inquiries, and the number of new accounts opened. MyFico.com offers helpful details.

Types of credit used: If your credit history has a mix of revolving loans and installment loans, generally this will improve your credit.

WECU members can view their free FICO® Score directly in Online and Mobile Banking! Simply log in or register, then scroll to the bottom of the Accounts tab.